July 3, 2026

July 3, 2026

Cashback credit cards are one of the easiest ways to save money on everyday purchases. Every eligible transaction—from grocery shopping and fuel purchases to dining and online shopping—can earn a percentage of your spending back as cash rewards. Over time, these rewards can add up to significant savings.

However, simply owning a cashback credit card doesn’t automatically maximize your benefits. To truly get the most value, you need to understand how cashback programs work and develop smart spending habits. The goal isn’t to spend more to earn rewards—it’s to earn more from the purchases you were already planning to make.

In this guide, we’ll explore seven practical cashback strategies that can help you maximize your savings while maintaining healthy financial habits.

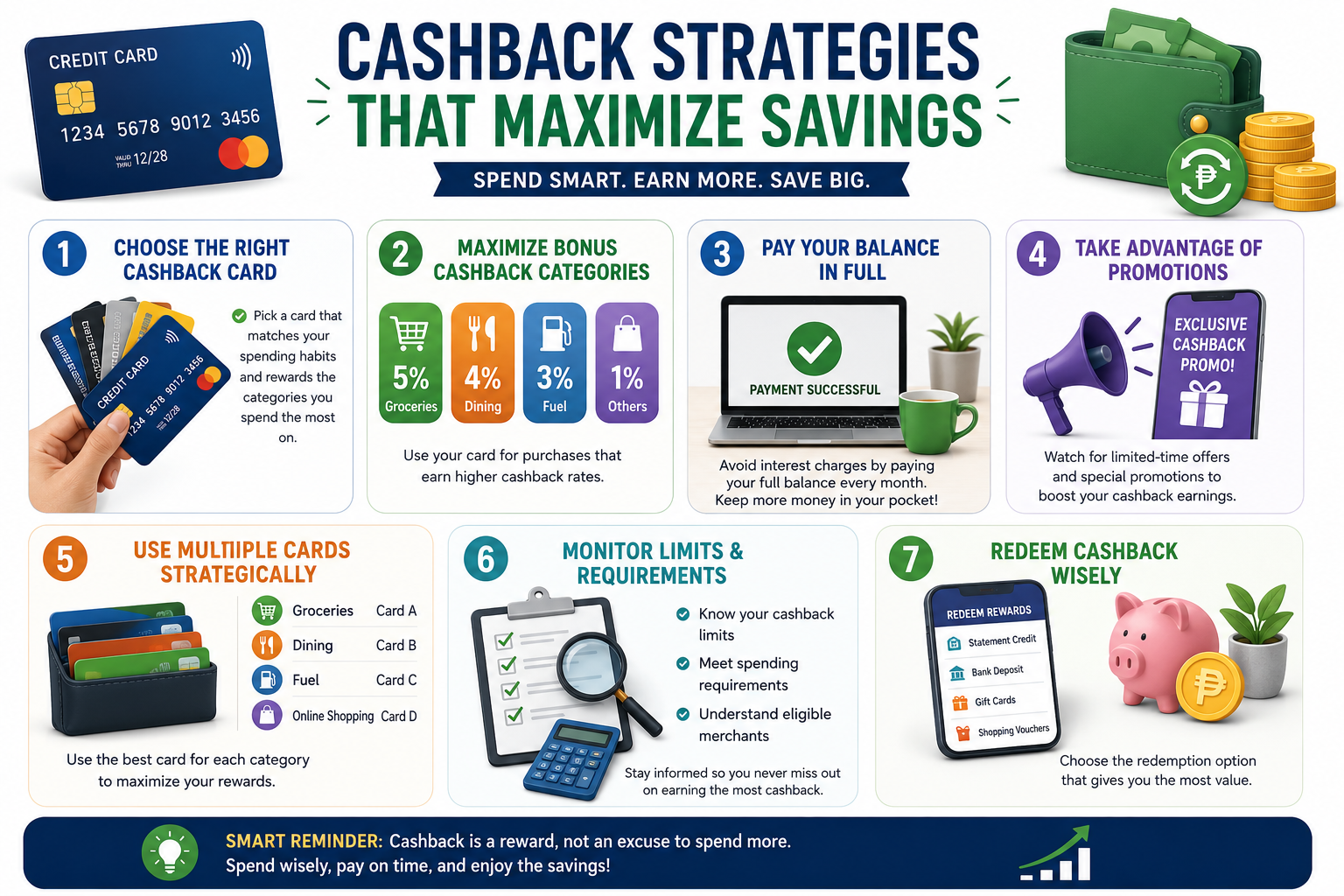

1. Choose a Cashback Card That Matches Your Spending Habits

Not all cashback credit cards reward the same spending categories.

Some offer higher cashback on:

- Groceries

- Dining

- Fuel

- Online shopping

- Utilities

- Travel

Others provide a flat cashback rate on every purchase.

Before applying for a card, review your monthly expenses and identify where you spend the most. Selecting a card that rewards your biggest spending categories can significantly increase your annual cashback earnings.

Example

If your family spends most of its monthly budget on groceries and utility bills, a cashback card with higher rewards in those categories will likely provide better value than one focused on travel.

2. Maximize Bonus Cashback Categories

Many cashback credit cards offer higher reward rates for selected categories.

For example:

| Spending Category | Cashback Rate |

|---|---|

| Groceries | 5% |

| Dining | 4% |

| Fuel | 3% |

| Other Purchases | 1% |

To maximize rewards:

- Use your cashback card whenever purchasing items within bonus categories.

- Plan recurring expenses around eligible merchants.

- Check if your bank has partner stores offering additional cashback promotions.

The more spending you direct toward high-reward categories, the more cashback you’ll accumulate.

3. Pay Your Balance in Full Every Month

One of the biggest mistakes people make is focusing only on cashback while ignoring interest charges.

Suppose you earn:

- ₱500 in cashback

But pay:

- ₱2,000 in interest

You’ve actually lost money.

The best way to maximize cashback is to avoid finance charges altogether by paying your statement balance in full every billing cycle.

Benefits include:

- No interest charges

- Better credit health

- Lower credit utilization

- More valuable rewards

4. Take Advantage of Limited-Time Promotions

Banks regularly launch promotional cashback campaigns throughout the year.

Examples include:

- Holiday shopping promotions

- Online shopping festivals

- Grocery partner discounts

- Dining cashback offers

- Fuel rebates

- Travel promotions

Before making larger purchases, check whether your credit card issuer is offering enhanced cashback.

Planning purchases around these promotions can substantially increase your savings without increasing your spending.

5. Use Multiple Cashback Cards Strategically

If you own more than one cashback credit card, you don’t necessarily have to use the same card for every purchase.

For example:

| Purchase | Best Card |

|---|---|

| Groceries | Card A |

| Fuel | Card B |

| Dining | Card C |

| Online Shopping | Card D |

Using the most rewarding card for each category allows you to maximize cashback across all your regular expenses.

However, be sure you can comfortably manage multiple payment due dates to avoid missed payments or unnecessary interest charges.

6. Monitor Cashback Limits and Spending Requirements

Many cashback programs include certain restrictions.

Common examples include:

Monthly Cashback Caps

Some cards limit the maximum cashback you can earn each month.

Minimum Spending Requirements

Certain bonus cashback rates only apply if you spend a minimum amount during the billing cycle.

Merchant Restrictions

Not every merchant qualifies for bonus cashback, even if it appears to belong to a qualifying category.

Understanding these rules helps ensure you’re earning the highest possible rewards without surprises.

7. Redeem Your Cashback Wisely

Different credit card issuers offer various redemption options.

Common choices include:

- Statement credits

- Bank deposits

- Shopping vouchers

- Gift cards

- Rewards portals

Choose the redemption method that offers the greatest value for your financial goals.

For many cardholders, applying cashback as a statement credit is one of the simplest ways to reduce future credit card balances.

Common Mistakes That Reduce Cashback Savings

Even experienced cardholders sometimes lose potential rewards by making avoidable mistakes.

Avoid these common pitfalls:

- Spending more simply to earn cashback

- Carrying high-interest balances

- Missing payment due dates

- Forgetting to redeem rewards

- Ignoring promotional offers

- Using the wrong card for bonus categories

Remember, cashback should complement responsible spending—not encourage unnecessary purchases.

Additional Tips for Maximizing Cashback

Beyond the seven strategies above, these habits can help you earn even more over time:

Automate Recurring Bills

If eligible, use your cashback card for recurring expenses such as:

- Internet

- Mobile phone

- Electricity

- Water

- Streaming subscriptions

These regular payments can generate consistent rewards every month.

Track Your Spending

Review your monthly statements to identify where most of your money goes. This helps ensure you’re using the most rewarding card for each purchase.

Stay Updated on New Offers

Banks frequently update their cashback programs, partner merchants, and promotional campaigns. Checking these offers regularly can help you maximize future rewards.

Who Benefits Most From Cashback Credit Cards?

Cashback credit cards are especially beneficial for people who:

- Pay their balances in full every month

- Have consistent monthly expenses

- Shop regularly for groceries

- Frequently dine out

- Purchase fuel often

- Shop online

- Want straightforward rewards instead of travel points

If your spending aligns with your card’s bonus categories, cashback can provide substantial value throughout the year.

Final Thoughts

Cashback credit cards can help you save money on everyday purchases, but maximizing those savings requires more than simply swiping your card. Choosing the right cashback card, focusing on bonus categories, paying your balance in full, taking advantage of promotions, and monitoring your rewards can significantly increase the value you receive.

The most successful cashback strategy is one that fits your existing lifestyle and budget. Rather than spending more to earn rewards, use your credit card strategically for planned purchases and always prioritize responsible financial habits. With the right approach, cashback rewards can become an easy and consistent way to reduce your everyday expenses while improving your overall financial well-being.