June 26, 2026

June 26, 2026

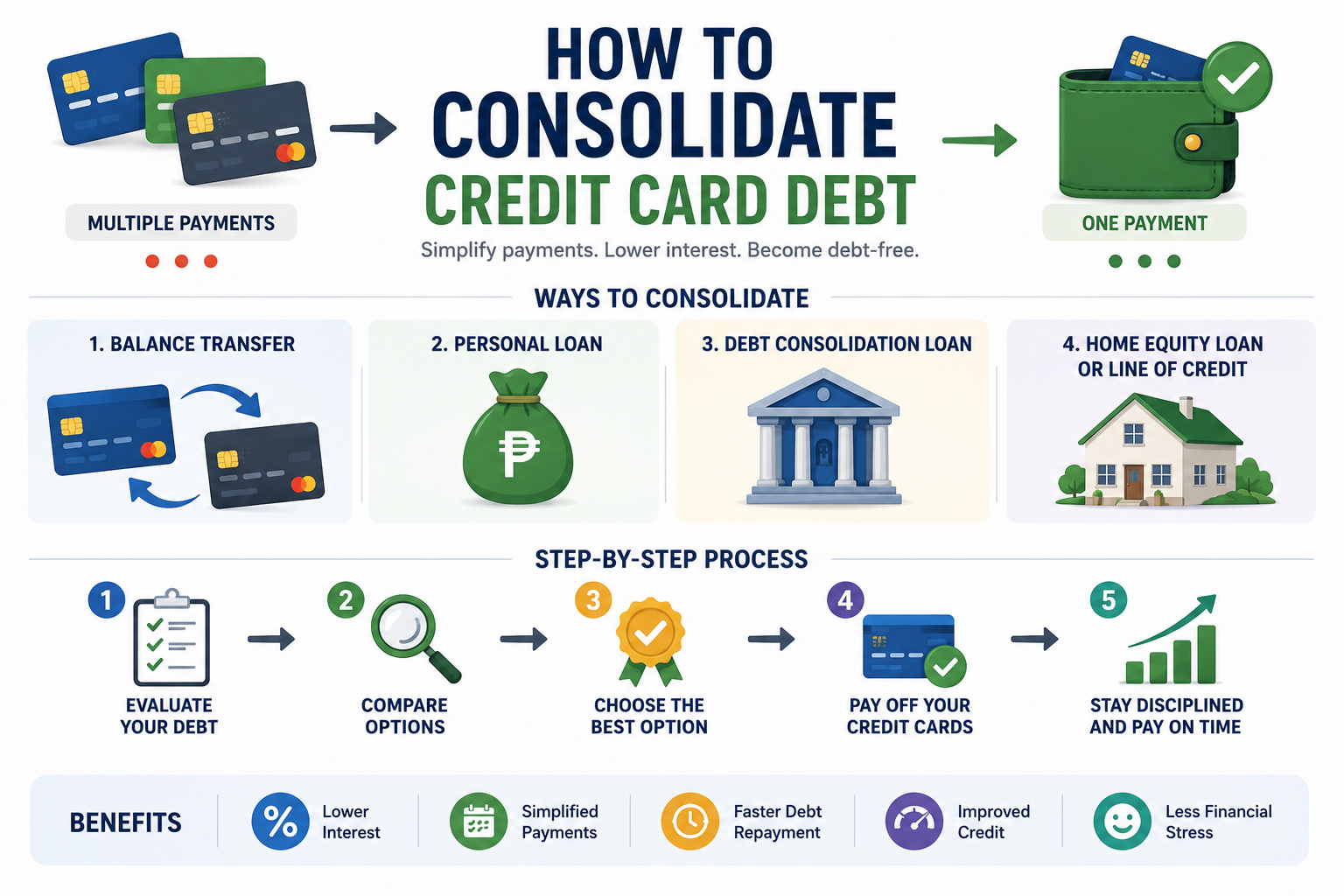

Managing multiple credit card balances can quickly become overwhelming. Different due dates, varying interest rates, and multiple monthly payments can make it difficult to stay on top of your finances. If you’re struggling to manage several credit card accounts, debt consolidation may be a practical solution.

Credit card debt consolidation combines multiple balances into a single payment, often with the goal of simplifying repayment and potentially reducing interest costs. While it isn’t a magic fix, it can be an effective strategy when combined with responsible spending habits and a solid repayment plan.

This guide explains how credit card debt consolidation works, its advantages and disadvantages, and the different options available to help you regain control of your finances.

What Is Credit Card Debt Consolidation?

Credit card debt consolidation is the process of combining multiple credit card balances into one loan or one credit account.

Instead of managing several monthly payments, you make a single payment according to the terms of the consolidation option you choose.

The primary goals are to:

- Simplify repayment

- Potentially lower interest costs

- Improve cash flow

- Reduce financial stress

- Create a structured repayment plan

Debt consolidation doesn’t eliminate debt—it simply changes how you repay it.

When Should You Consider Debt Consolidation?

Debt consolidation may be worth considering if you:

- Have multiple credit card balances

- Are paying high interest rates

- Find it difficult to manage several due dates

- Consistently carry balances every month

- Want a more organized repayment strategy

However, consolidation works best for individuals who are committed to avoiding new debt while paying off existing balances.

Benefits of Consolidating Credit Card Debt

There are several advantages to consolidating your credit card balances.

1. One Monthly Payment

Instead of remembering several payment dates, you’ll typically make one monthly payment.

This makes budgeting easier and reduces the risk of missed payments.

2. Potentially Lower Interest Costs

Depending on the consolidation method, you may qualify for a lower interest rate than your current credit cards.

Lower interest means more of your payment goes toward reducing the principal balance.

3. Easier Budget Management

Managing one payment simplifies your monthly budget and helps you better track your financial progress.

4. Reduced Financial Stress

Many borrowers feel less overwhelmed after replacing multiple debts with a single repayment plan.

Common Ways to Consolidate Credit Card Debt

1. Balance Transfer Credit Cards

A balance transfer allows you to move balances from one or more credit cards to another card.

Some balance transfer programs offer promotional interest rates for a limited period.

Advantages

- Potentially lower interest

- Faster debt repayment

- One account to manage

Considerations

- Balance transfer fees may apply.

- Promotional rates eventually expire.

- Approval depends on your credit profile.

2. Personal Loans

Many borrowers use personal loans to pay off multiple credit cards.

After receiving the loan, you pay off your credit cards and then repay the personal loan through fixed monthly installments.

Advantages

- Predictable monthly payments

- Fixed repayment schedule

- Potentially lower interest

Considerations

- Loan approval requirements

- Possible processing fees

- Interest rates vary by lender

3. Home Equity Loans (Where Applicable)

Homeowners with sufficient equity may qualify for home equity financing.

Because these loans are secured by property, they often carry lower interest rates than unsecured credit cards.

However, failing to repay the loan may put your property at risk.

This option should only be considered after careful financial evaluation.

4. Debt Management Programs

Some nonprofit credit counseling organizations offer structured debt management plans.

These programs may:

- Negotiate with creditors

- Simplify payments

- Provide financial education

- Create realistic repayment schedules

Debt management programs can be helpful for borrowers experiencing significant financial challenges.

How to Consolidate Credit Card Debt

Step 1: Calculate Your Total Debt

Begin by listing every credit card balance.

Include:

- Outstanding balance

- Interest rate

- Minimum payment

- Due date

Knowing exactly how much you owe helps determine which consolidation method is most appropriate.

Step 2: Review Your Credit Standing

Your credit profile may affect which consolidation options are available.

A stronger credit history often provides access to:

- Lower interest rates

- Better loan terms

- Higher approval odds

If your credit score needs improvement, you may wish to strengthen it before applying.

Step 3: Compare Consolidation Options

Don’t accept the first offer you receive.

Compare:

- Interest rates

- Fees

- Repayment periods

- Monthly payment amounts

- Total borrowing costs

The lowest monthly payment isn’t always the least expensive option over time.

Step 4: Create a Repayment Budget

Once you’ve consolidated your debt, develop a realistic monthly budget.

Include:

- Essential living expenses

- Debt payments

- Savings contributions

- Emergency fund goals

Following a budget reduces the likelihood of accumulating new debt.

Step 5: Avoid Using Paid-Off Credit Cards

One of the biggest mistakes borrowers make is continuing to use credit cards after consolidating debt.

If new balances accumulate while you’re repaying the consolidation loan, your debt situation can become even worse.

Consider:

- Using cash for discretionary purchases

- Paying with debit cards

- Limiting credit card spending until debt is under control

Mistakes to Avoid

When consolidating credit card debt, avoid these common mistakes:

Borrowing Without a Repayment Plan

Consolidation should support a structured repayment strategy.

Ignoring Fees

Review all:

- Processing fees

- Transfer fees

- Annual fees

- Early repayment penalties

Continuing to Overspend

Consolidation only works if spending habits improve.

Choosing Longer Terms Without Calculating Total Cost

Lower monthly payments may result in paying more interest over time.

Is Debt Consolidation Right for Everyone?

Not necessarily.

Debt consolidation works best if you:

- Have steady income

- Can consistently make monthly payments

- Are committed to reducing debt

- Avoid accumulating new balances

If spending habits remain unchanged, consolidation alone will not solve the underlying problem.

Alternatives to Debt Consolidation

Depending on your situation, other strategies may be more appropriate.

These include:

Debt Snowball Method

Pay off the smallest balance first to build momentum.

Debt Avalanche Method

Prioritize the highest-interest balance to reduce total interest costs.

Increasing Your Income

Additional income from freelancing, overtime, or part-time work can accelerate repayment.

Negotiating With Creditors

Some lenders may offer hardship programs or temporary payment arrangements.

Tips for Staying Debt-Free After Consolidation

Successfully consolidating your debt is only the beginning.

Maintain healthy financial habits by:

- Paying every bill on time

- Keeping credit utilization low

- Monitoring your monthly spending

- Building an emergency fund

- Reviewing your credit report regularly

- Using credit cards responsibly

- Avoiding unnecessary debt

Long-term financial success depends on consistent money management—not just eliminating current balances.

Final Thoughts

Credit card debt consolidation can be an effective way to simplify your finances, reduce stress, and create a clear path toward becoming debt-free. Whether you choose a balance transfer, personal loan, or another consolidation method, the key is selecting an option that aligns with your financial situation and committing to responsible repayment.

Remember that consolidation is a tool—not a complete solution. Lasting financial improvement comes from budgeting wisely, controlling spending, paying on time, and avoiding new debt. Combined with healthy financial habits, debt consolidation can help you regain control of your finances and move closer to long-term financial freedom.