June 18, 2026

June 18, 2026

Many people assume that closing a credit card is always a positive financial move, especially if they no longer use the account or want to simplify their finances. While there are situations where closing a credit card makes sense, it’s important to understand that doing so can sometimes have unintended consequences for your credit score.

Your credit score is influenced by several factors, including your payment history, credit utilization, length of credit history, and overall credit profile. Closing a credit card can affect some of these factors, potentially impacting your credit standing.

Before deciding to close a credit card account, it’s worth understanding how the process works and what effect it may have on your financial health.

Why People Close Credit Cards

There are many reasons why someone may choose to close a credit card.

Common reasons include:

- Avoiding credit card annual fees

- Simplifying finances

- Reducing the temptation to overspend

- Switching to a better credit card

- Ending unused accounts

- Resolving concerns about fraud or security

While these reasons may be valid, it’s important to evaluate the potential impact on your credit profile before taking action.

How Credit Scores Are Calculated

To understand how closing a credit card can affect your score, it helps to know some of the major factors lenders consider.

These typically include:

- Payment history

- Credit utilization

- Length of credit history

- Credit mix

- Recent credit activity

Closing a card doesn’t affect all of these factors equally, but it can influence several important areas.

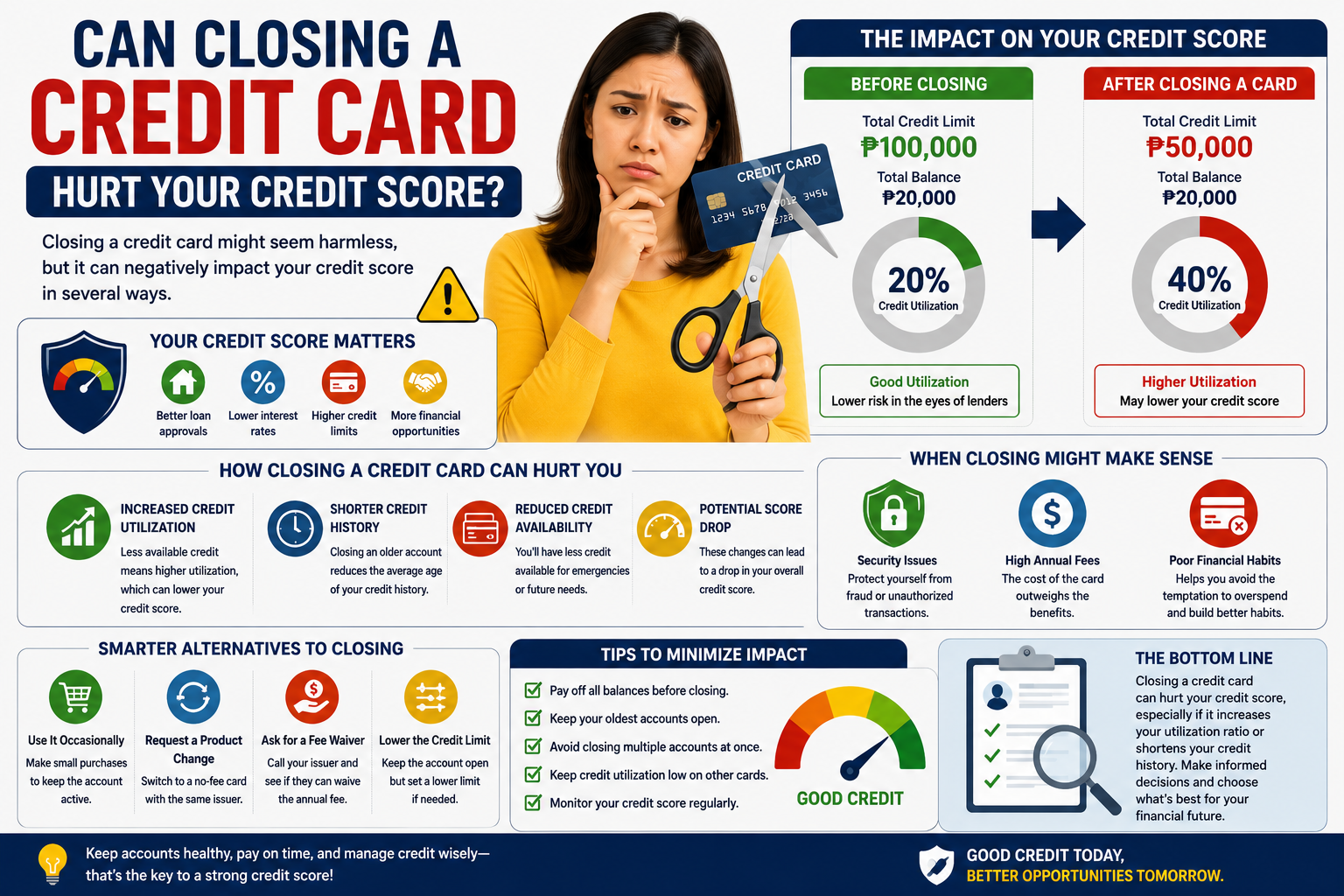

Credit Utilization May Increase

One of the most significant ways closing a credit card can affect your score is through credit utilization.

Credit utilization measures how much of your available credit you’re using.

For example:

- Card A limit: ₱50,000

- Card B limit: ₱50,000

- Total available credit: ₱100,000

- Total balance: ₱20,000

Your utilization ratio is:

20%

Now imagine you close Card B.

- Remaining available credit: ₱50,000

- Existing balance: ₱20,000

Your utilization ratio increases to:

40%

Even though your spending hasn’t changed, your utilization has doubled because your available credit decreased.

Higher utilization ratios can negatively affect your credit score because they may signal increased reliance on credit.

Closing an Older Account May Affect Credit History

The age of your credit accounts contributes to your overall credit profile.

Older accounts demonstrate a longer history of responsible credit management.

If you close one of your oldest credit cards, lenders may eventually have less historical information to evaluate.

While the impact may not be immediate, losing an established account can potentially weaken the strength of your overall credit history over time.

This is especially important for individuals with relatively few credit accounts.

Your Payment History Usually Remains

One common misconception is that closing a credit card immediately erases its history.

In reality, positive account history may continue to remain part of your credit record for a period of time, depending on reporting practices and regulations.

This means that years of responsible payments don’t simply disappear overnight when an account is closed.

However, maintaining active accounts in good standing can continue contributing to a healthy credit profile.

Closing a Card May Reduce Financial Flexibility

A credit card can serve as a financial safety net during emergencies.

Closing an account may reduce:

- Available credit

- Emergency spending capacity

- Purchasing flexibility

- Backup payment options

While this doesn’t directly determine your credit score, it can influence your overall financial resilience.

When Closing a Credit Card Makes Sense

Despite the potential drawbacks, there are situations where closing a credit card may still be a reasonable decision.

High Annual Fees

If a card’s annual fee outweighs its benefits, closing the account may save money.

Fraud or Security Concerns

If an account has experienced repeated security issues, closure may be appropriate.

Joint Accounts After Major Life Changes

In certain situations, closing shared accounts may be necessary for financial separation.

Poor Financial Habits

If access to a particular card encourages excessive spending, closing it may support better financial management.

The key is weighing these benefits against the possible effects on your credit profile.

When You Should Think Twice Before Closing a Card

There are certain situations where keeping a card open may be the better option.

It Is Your Oldest Account

Older accounts often contribute positively to your credit history.

It Has No Annual Fee

If the card costs nothing to keep, maintaining the account may benefit your credit profile.

It Provides Significant Available Credit

Closing a high-limit card can significantly increase your utilization ratio.

You Have Few Credit Accounts

Individuals with limited credit histories may experience a greater impact from account closures.

Alternatives to Closing a Credit Card

If you’re unsure about closing an account, consider these alternatives.

Use It Occasionally

Making a small purchase every few months can help keep the account active.

Request a Product Change

Some issuers allow you to switch to a different card without closing the account.

Negotiate Fee Waivers

In some cases, issuers may reduce or waive annual fees to retain customers.

Lower Spending Limits Voluntarily

If overspending is a concern, reducing the available limit may help while preserving account history.

How to Minimize Credit Score Impact

If you decide to close a credit card, consider the following strategies:

Pay Off Outstanding Balances First

Avoid carrying balances on the account you’re closing.

Reduce Balances on Other Cards

Lower utilization elsewhere can offset the loss of available credit.

Keep Older Accounts Open

Preserving long-standing accounts may help maintain credit history.

Avoid Multiple Closures at Once

Closing several accounts simultaneously may create a larger impact.

Monitor Your Credit Profile

Regular monitoring allows you to track any changes after account closure.

Common Myths About Closing Credit Cards

Myth 1: Closing a Card Always Improves Your Credit Score

In many cases, the opposite may occur due to increased utilization.

Myth 2: Unused Cards Automatically Hurt Your Credit

Unused cards don’t necessarily damage your credit if they’re managed responsibly.

Myth 3: Closing a Card Erases Its History Immediately

Account history typically remains visible for some time after closure.

Myth 4: You Should Close Every Card You Don’t Use

Sometimes maintaining an older, fee-free account may be beneficial.

Final Thoughts

Closing a credit card can affect your credit score, particularly if it increases your credit utilization ratio or reduces the average age of your credit accounts. While there are situations where closing a card makes financial sense, it’s important to carefully consider the potential impact before making a decision.

If the card has no annual fee, contributes significantly to your available credit, or represents one of your oldest accounts, keeping it open may help support a stronger credit profile. On the other hand, if the card no longer serves your financial needs or carries costly fees, closing it may still be the right choice.

Ultimately, maintaining healthy credit habits—including paying bills on time, keeping balances low, and managing accounts responsibly—will have a far greater influence on your credit standing than any single account closure.