June 10, 2026

June 10, 2026

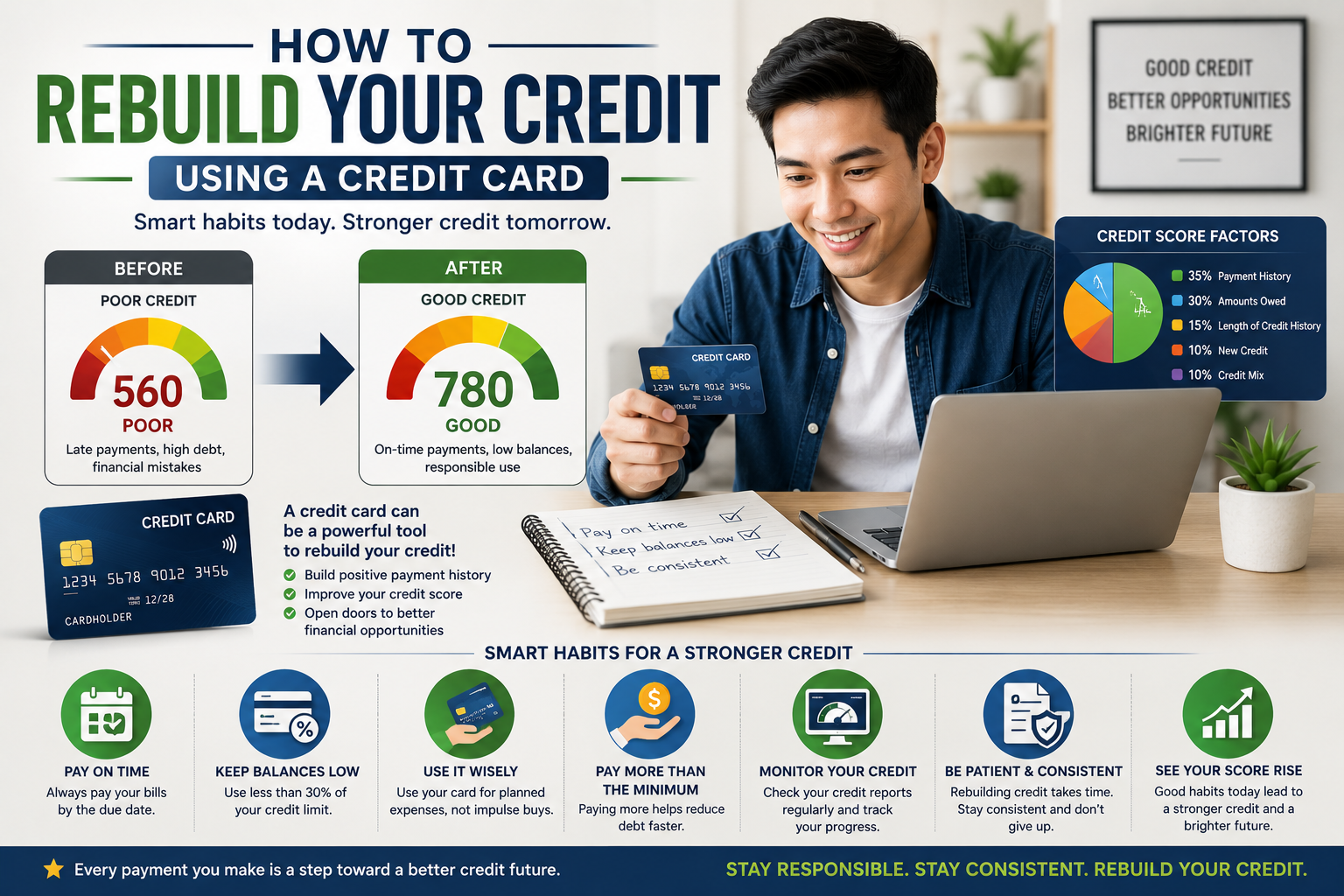

A damaged credit history can make it more difficult to qualify for loans, mortgages, and even new credit cards. Whether your credit score has been affected by missed payments, high debt levels, financial hardship, or past mistakes, the good news is that rebuilding your credit is possible.

One of the most effective tools for restoring your credit profile is a credit card. When used responsibly, a credit card can demonstrate positive financial behavior to lenders and help improve your credit standing over time.

In this guide, we’ll explore how you can use a credit card strategically to rebuild your credit and create a stronger financial future.

Understanding Credit Rebuilding

Credit rebuilding is the process of improving your creditworthiness after experiencing negative credit events.

These may include:

- Late payments

- Loan defaults

- High credit utilization

- Collections accounts

- Bankruptcy or financial hardship

- Limited credit history

While negative marks may remain on your credit report for several years, positive financial habits can gradually offset their impact and help restore lender confidence.

Why a Credit Card Can Help Rebuild Credit

Credit cards provide ongoing opportunities to demonstrate responsible credit management.

When you consistently:

- Make payments on time

- Keep balances low

- Maintain accounts in good standing

You establish positive activity that can strengthen your credit profile over time.

Unlike some financial products, credit cards allow you to build a continuous record of responsible borrowing behavior month after month.

Start with the Right Credit Card

Not every credit card is ideal for credit rebuilding.

Secured Credit Cards

A secured credit card is often one of the best options for individuals with damaged or limited credit histories.

These cards typically require a refundable security deposit, which serves as collateral.

Benefits include:

- Easier approval requirements

- Opportunity to build positive payment history

- Lower risk for lenders

- Pathway to traditional unsecured cards

Entry-Level Credit Cards

Some financial institutions offer basic credit cards designed for individuals looking to establish or rebuild credit.

These cards may have:

- Lower credit limits

- Simplified approval requirements

- Basic rewards programs

- Credit-building opportunities

Make Every Payment on Time

Payment history is often the most influential factor in determining credit standing.

Missing payments can significantly delay your progress.

To ensure consistent payments:

- Set up automatic payments.

- Schedule reminders on your phone.

- Pay as soon as your statement becomes available.

- Link payments to your regular payday schedule.

Even one missed payment can negatively affect months of progress.

Keep Credit Utilization Low

Credit utilization refers to the percentage of your available credit that you’re currently using.

For example:

- Credit limit: ₱50,000

- Current balance: ₱10,000

- Utilization rate: 20%

Financial experts generally recommend keeping credit utilization below 30%, while lower percentages are even better.

High utilization may signal financial stress, even if you make payments on time.

Practical Tips

- Use your card for small purchases.

- Avoid maxing out your credit limit.

- Make multiple payments during the month.

- Pay balances before the statement closing date.

Use Your Card Regularly—but Responsibly

One common mistake is opening a credit card and rarely using it.

Lenders want to see active, responsible credit management.

Good uses for a rebuilding credit card include:

- Utility bills

- Streaming subscriptions

- Groceries

- Fuel expenses

- Small recurring purchases

The goal is to generate positive payment activity without accumulating unnecessary debt.

Pay More Than the Minimum Due

While making minimum payments keeps your account current, paying your balance in full offers greater benefits.

Advantages include:

- Lower interest charges

- Faster debt reduction

- Better credit utilization

- Stronger financial discipline

Whenever possible, aim to pay the entire balance before the due date.

Avoid Applying for Multiple Credit Cards

Many people rebuilding credit mistakenly believe that opening several accounts will speed up the process.

In reality, excessive applications can:

- Generate multiple credit inquiries

- Increase lender concerns

- Lower approval odds

- Complicate financial management

Focus on managing one card successfully before considering additional accounts.

Monitor Your Credit Progress

Tracking your credit profile helps you understand how your actions affect your financial standing.

Regular monitoring allows you to:

- Identify errors

- Detect fraudulent activity

- Measure improvement

- Stay motivated throughout the rebuilding process

Reviewing your credit reports periodically can help ensure that all information is accurate and current.

Maintain Older Accounts

The length of your credit history contributes to your overall credit profile.

If you have older accounts in good standing, keeping them open may benefit your credit standing.

Older accounts can:

- Increase average account age

- Improve credit history length

- Demonstrate long-term financial responsibility

Closing old accounts without a compelling reason may reduce these advantages.

Create a Budget to Support Credit Rebuilding

A realistic budget can prevent overspending and help ensure that you always have funds available for payments.

Your budget should include:

- Monthly income

- Essential expenses

- Debt repayment goals

- Savings contributions

- Credit card spending limits

Financial discipline is one of the strongest foundations for successful credit rebuilding.

Be Patient and Consistent

Rebuilding credit is not an overnight process.

Depending on the severity of past credit issues, noticeable improvements may take several months or even years.

However, consistent positive behavior can gradually outweigh previous mistakes.

Focus on:

- Paying on time

- Maintaining low balances

- Avoiding unnecessary debt

- Using credit responsibly

Small improvements made consistently often produce significant long-term results.

Common Mistakes to Avoid

When rebuilding your credit, avoid these common pitfalls:

Missing Payments

Payment history remains one of the most important credit factors.

Maxing Out Credit Cards

High utilization can quickly undermine progress.

Applying for Too Much Credit

Frequent applications may signal financial instability.

Ignoring Account Statements

Regularly reviewing statements helps identify issues early.

Closing Accounts Too Soon

Maintaining older accounts can support your credit profile.

Signs Your Credit Is Improving

As your efforts begin to pay off, you may notice:

- Higher credit scores

- Improved approval odds

- Lower interest rates

- Increased credit limits

- Better financial opportunities

These milestones indicate that lenders are gaining confidence in your ability to manage credit responsibly.

Final Thoughts

A credit card can be one of the most effective tools for rebuilding your credit when used strategically and responsibly. By choosing the right card, making on-time payments, keeping utilization low, monitoring your progress, and maintaining healthy financial habits, you can gradually strengthen your credit profile.

The journey may require patience, but every responsible payment and smart financial decision moves you closer to a stronger credit standing. Over time, these efforts can open the door to better borrowing opportunities, greater financial flexibility, and long-term financial success.